Produced by Activate Group in collaboration with Gecko Risk.

This edition focuses on key developments in 2024, highlighting the growth in EV registrations, evolving trends in repair costs, and the impact of new entrants on the market.

The start of 2025 has been a turbulent time for the electric vehicle (EV) sector, with major policy and market developments shaping the conversation. In March, the UK Government announced plans to relax annual EV sales targets, while manufacturers of all vehicle types reacted to the news of increased tariffs from the United States on vehicles and parts.

While these changes signal a shifting policy landscape, the impact has yet to be seen in the UK’s registration data. Q1 figures show continued strength in EV adoption, with 120,000 new battery electric vehicles registered, accounting for 20% of all new vehicles.

Produced by Activate Group in collaboration with Gecko Risk, this quarterly report explores key developments across registrations and repair trends, offering a snapshot of the UK EV market as it stands—and what may lie ahead.

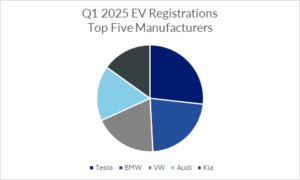

The first quarter saw some changes among the top-selling EV manufacturers. Tesla remained the most popular EV brand in the UK, though BMW is now a close second and increasingly challenging Tesla’s long-standing dominance. Kia also performed strongly, in Q1, securing fifth position in the EV rankings thanks to the popularity of its EV3 model.

Chinese manufacturer BYD made its debut in the UK’s top ten, registering 5,297 vehicles in Q1—an impressive leap compared to just 1,278 registrations during the same period last year. This significant growth highlights the increasing competitiveness of new entrants in the market and the appeal of more affordable EV options.

James Fisher, CEO of Gecko Risk, commented:

“In early March, the Prime Minister announced plans to ease annual EV sales targets to support car manufacturers facing tough US tariffs. Despite this, March was a record-breaking month for EV registrations in the UK, with over 69,000 new electric cars and nearly 4,000 electric vans hitting the road.

“Tesla remained the top-selling EV brand in March, with more than 7,000 new registrations. While their share price has taken a hit recently, many of these cars were likely ordered months ago, and it will be interesting to follow the trend in Tesla registrations over the months ahead.”

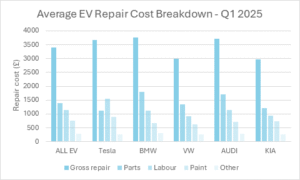

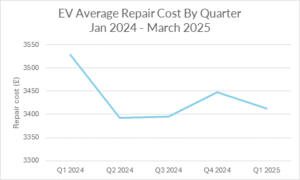

Average EV repair costs remained stable in Q1, falling slightly to £3,412 compared to £3,447 in Q4 2024. This figure also represents a 3.3% year-on-year decrease, with average costs sitting at £3,528 during the same quarter in 2024.

Adrian Furness, Managing Director of Activate Group’s insurance division, commented on the stability in EV repair costs:

“We’re seeing a more stable picture when it comes to EV repair costs, and that’s a result of the growing number of EVs in the UK car parc.

“With more of these vehicles on the road, parts availability has improved, and more repairers are now fully trained and certified to work on EVs.

“Insurers are also getting smarter with how they assess EV risk, and better use of AI and repair tech is making the process more efficient overall. These factors are contributing to a more balanced, manageable cost landscape.”

Parts costs were largely consistent with Q1 2024, while a reduction in labour rates helped drive down overall repair costs. However, one upward trend has persisted: paint costs have been rising gradually since 2022 and continued to increase in Q1 2025. This has been attributed to rising raw material prices, and greater complexity in EV paint finishes.

Repair costs for premium brands such as Tesla, Audi and BMW remain higher than average, which is expected given their positioning in the market. In contrast, brands like VW and Kia show lower average repair costs, reflecting their more accessible pricing.

As in ICE repairs, parts continue to make up the largest share of EV repair costs for most brands. Typically, parts account for around 45% of the total repair bill. However, Tesla deviates from this trend, with labour comprising the more significant portion of the cost – in Q1, parts represented just 30% of Tesla’s average repair cost. The same pattern is noticeable among Chinese-owned brands such as MG and BYD, setting them apart from established, European manufacturers.

The first quarter of 2025 reflects a maturing EV market—characterised by stable repair costs, growing consumer adoption, and increased competition among both established and emerging manufacturers. While recent policy shifts and global trade challenges have introduced new uncertainties, their impact has yet to ripple through UK registration or repair data in any significant way.

Looking ahead, the next quarter will begin to reveal how changes to EV sales targets, consumer attitudes and international tariffs may influence EV registrations.

Activate Group and Gecko Risk will continue to monitor these developments closely, providing insight into how evolving market forces shape the future of the EV sector.

Activate Group and its subsidiaries provide end-to-end accident management solutions to insurers, fleet providers, TPAs and brokers. The group provides claims management to corporate and commercial fleets through sopp+sopp, operates an approved nationwide repair network for personal lines insurance claims through Motor Repair Network, supplies next-day parts and consumables through Activate Parts and also runs its own body shop division, Activate Accident Repair. Based in the UK, Activate Group employs more than 800 people.