Vehicles on the Road Data – May 2025

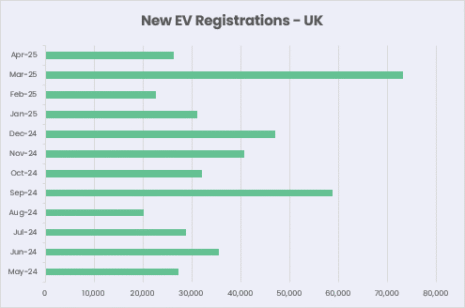

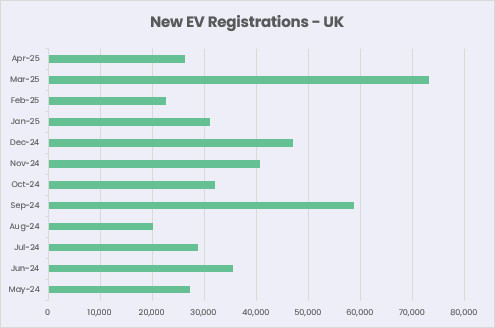

SMMT have reported a year on year 10.4% decrease for all new vehicle registrations for the month of April. This downward trend has been evident for most of the last six months, which can most likely be put down to damaged consumer confidence in the current economic climate. However, we have noted that BEV new registrations buck the trend, with an increase of almost 11% year on year. In April 2024 new BEV new registrations stood at 23,578 whereas last month we recorded 26,168 vehicles. Admittedly, BEV new registrations are no doubt helped by very attractive salary sacrifice schemes.

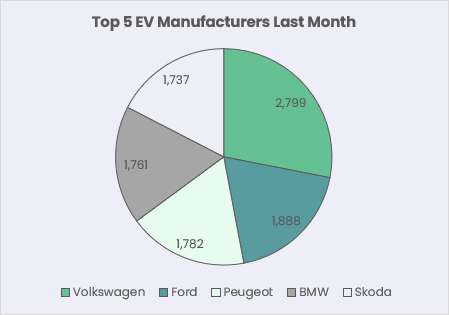

Perhaps the most notable stat we have picked up from last month is that Tesla new registrations are the lowest they have been for well over year. This could be down to a combination of factors, such as increased competition from both new and legacy manufacturers as well as potential customers having their heads turned from away the Tesla brand due to Elon Musk’s political controversies.

Tesla not only dropped out of the top 5 manufacturers in April, but in fact fell down to 18th place. It was not only Tesla who moved out of the top 5, with both Audi and Kia being relegated. They were replaced by Ford, Peugeot and new entrants Skoda. Elsewhere, BYD continue to be making inroads with 1,405 new BEV registrations in April, almost three times that of which Tesla recorded last month.

Repair Costs Data

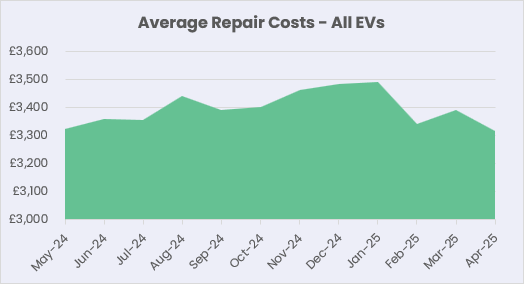

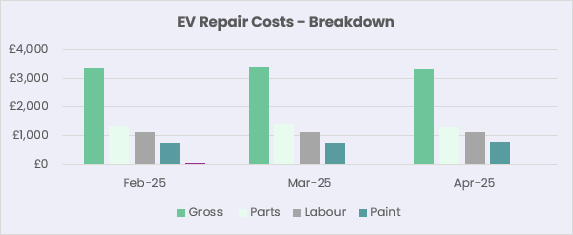

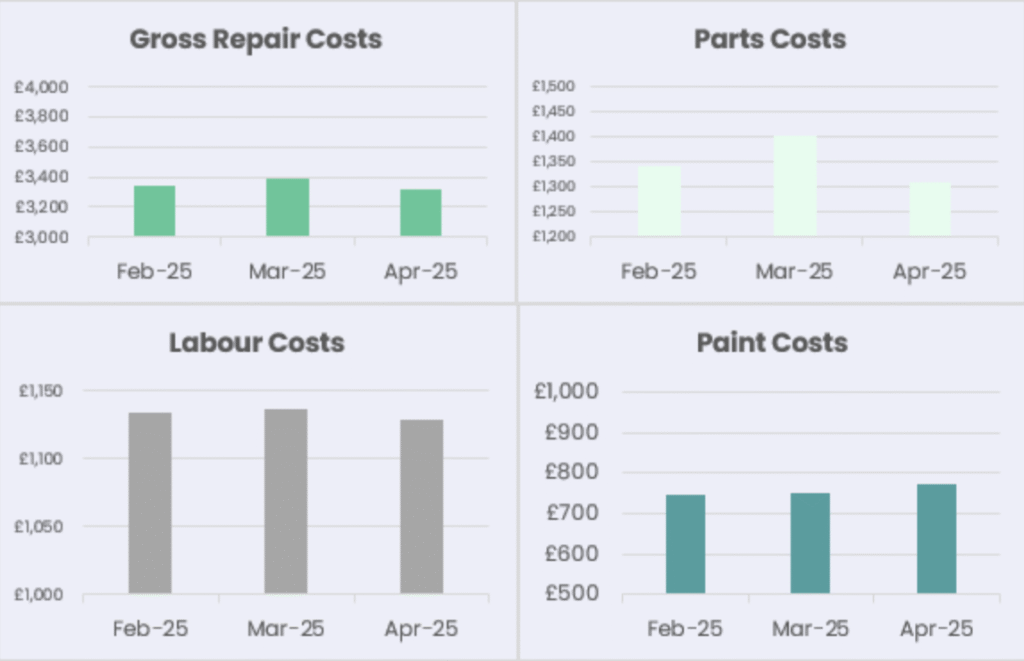

Average BEV repair costs for the month of April-2025 are the lowest they have been for three years and are over 5% down from the start of 2025. This seems to be driven by Parts Costs coming down, whereas Labour and Paint Costs appear to have been steadier. We have seen a trend of Parts Costs being lower for new manufacturers, so perhaps as the market share of non-legacy manufacturers increases, this helps to push Gross Repair Costs down.

Repair Costs – Top 5 Manufacturers by New Registrations (last 12 months)

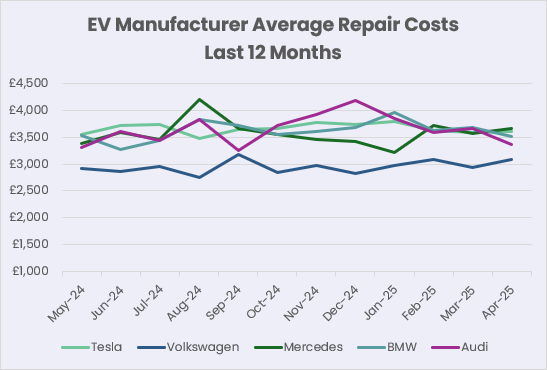

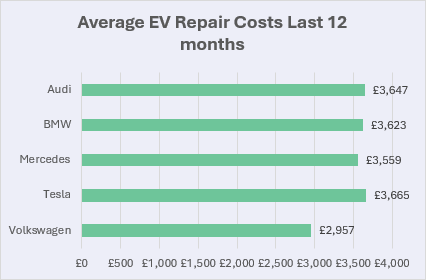

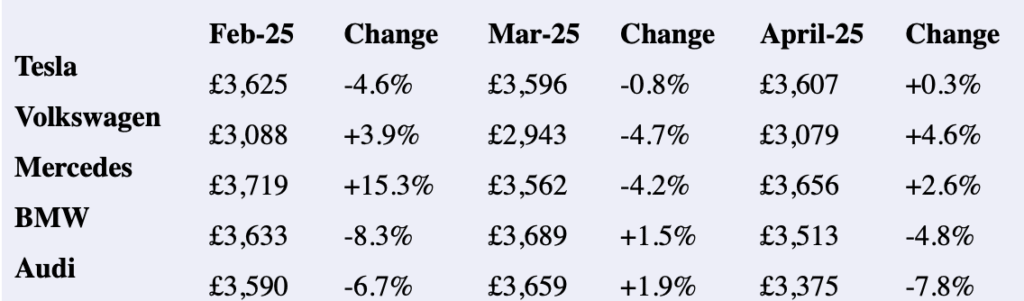

Following the trend from the previous month there has been very little separating average Repair Costs for BMW, Mercedes and Tesla. However, Audi’s average Repair Costs dropped by 7.8%, bringing them below that of their main rivals. It will be interesting to see if they can maintain this going forward.

Average repair costs for Volkswagen continue to be between 15-20% lower than that of the four other core manufacturers we report on. However, for similarly valued manufacturers to Volkswagen, such as Cupra, Nissan and Kia, average Repair Costs have been little more than £50 apart over the last 12 months. Interestingly, Volvo holds a lower average Repair Cost over this period (£2,897) than all of the above manufacturers.

On a make level there appears to be less volatility when it comes to repair costs across the board. We understand this is due to increased capacity as well bodyshops being more up to speed with their manufacturer approvals and improved EV diagnostics. We do however understand that battery diagnostics and write offs due to any kind of battery damage continue to be a critical area of concern throughout the whole mobility sector.

Obviously, this is an area that needs addressing, however, we were encouraged to see a report by Arval into battery longevity. Following extensive testing of over 8,000 vehicles for more than an 18 month period in 8 different countries, they found that the average battery health after driving 43,000 miles was 93%, while after 124,000 miles the average remained close to 90%. All the more reason to get battery diagnostics and repairs right!

Average Repair Costs by Manufacturer – Last 3 Months

n.b. Repair Costs are inclusive of discounts, but excluding tax.

To find out more about Gecko Risk and gain access to more in depth new energy vehicle data, please contact team@geckorisk.com